Market Recap – Week Ending Nov. 22

Stocks Climb; PCE Report on Wednesday

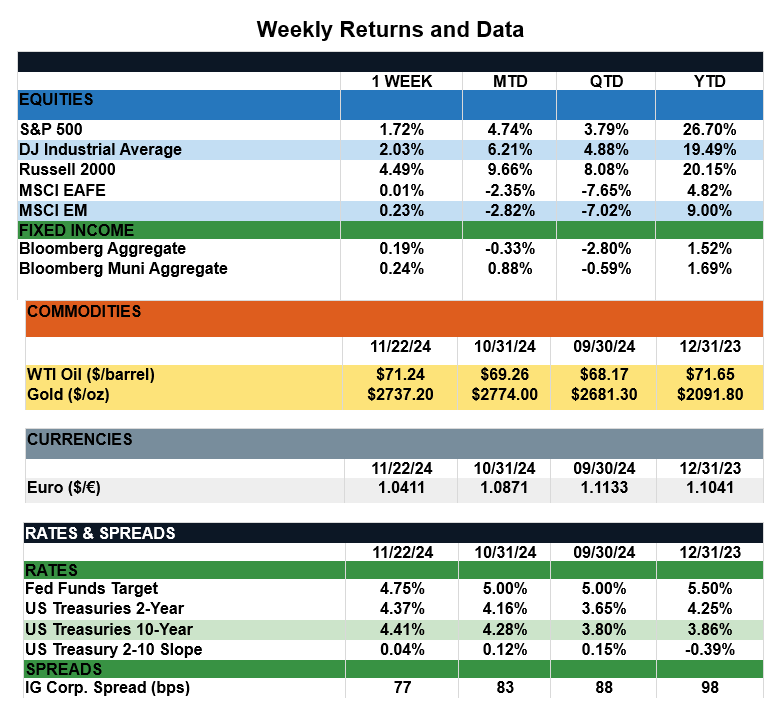

Overview: Global stocks traded higher last week as strong earnings in the U.S. continued to fuel investor optimism. In the U.S., the S&P 500 gained 1.7% in total return, while the Russell 2000 (small cap index) rallied nearly 4.5%. Overseas, international returns were suppressed by a stronger U.S. dollar, leaving the MSCI EAFE index higher by just 0.01% on the week. Meanwhile, Treasury yields were mixed last week as investors reacted to geopolitical tensions alongside a more hawkish Federal Reserve. All told, the Bloomberg Aggregate (taxable bond index) rose 0.2% for the week. On the commodities front, gold snapped its three-week losing streak, finishing the week higher by more than 5%. On the data front, U.S. Manufacturing PMI remained in contraction for November at a level 48.8, while services PMI surged from 55 to 57 for November (a reading above 50 indicates expansion, while a reading below 50 indicates contraction). Separately, higher interest rates continued to weigh on new housing in the U.S., as housing starts declined 3.1% in October. Looking forward to the week ahead, Wednesday will bring the second estimate of third-quarter real GDP growth, which is expected to remain unchanged at 2.8%. More importantly, investors will be focused on the PCE inflation report on Wednesday as well, which is the Fed’s preferred measure of inflation. The markets are expecting the Core PCE Price index to remain unchanged for October at 0.3% monthly, corresponding to year-over-year core inflation of 2.8%.

Update on Consumer Spending (from JP Morgan): This Thanksgiving, as families gather around the table, the festivities provide a welcome reprieve from the political tensions of recent months. With Americans expected to spend nearly a trillion dollars spreading holiday cheer, this spending showcases their resilience in a shifting economic landscape. While holiday spending is projected by the National Retail Federation to hit a record high, sales growth, is expected to fall slightly below the pre-pandemic average of 3.6%. However, this moderation reflects easing inflation rather than weakening demand. In fact, when adjusted for inflation, real sales are set to exceed last year, buoyed by record shopper turnout and an anticipated rise in per-person spending to around $900. Driving this is real wage growth, which has remained positive for a year and a half. Furthermore, stock market gains and recent Fed rate cuts have lifted consumer confidence. That said, elevated prices, along with the depletion of pandemic-era savings cushions, may cap spending growth for some households. Retailers, for whom the holiday season drives a disproportionate share of annual sales, face a mixed outlook. Deal-hunting consumers are turning to discount retailers, boosting revenue and profit forecasts. Conversely, those reliant on discretionary categories like apparel and specialty goods are seeing softer demand as shoppers focus on essentials. Despite challenges, this season reflects a broader economic trend: slowing but not stalling. As winter sets in, consumer spending is cooling but remains far from frosty - underscoring the resilience of the U.S. economy as we head into 2025.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Factset, CNBC.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.