Market Recap – Week Ending Aug. 23

Stocks Climb; Fed Comments Signal Interest-Rate Cuts

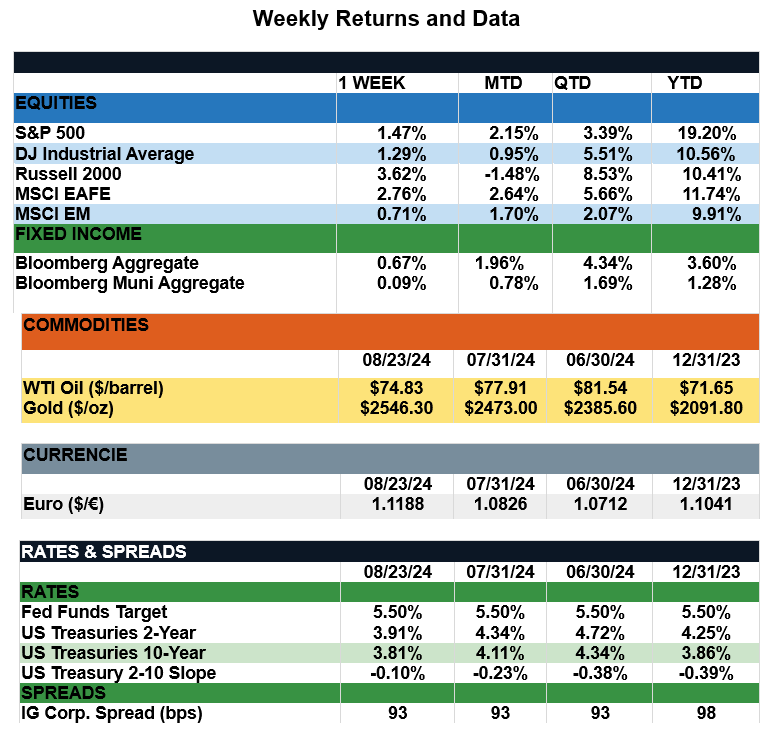

Overview: Stocks rose across the globe last week with international developed markets (MSCI EAFE) leading the way, up 2.8% on the week. Here in the U.S., the S&P 500 index closed the week 1.5% higher, and now is trading less than 1% away from its record high set in mid-July. The rally in stocks has extended to smaller companies as well with the small cap Russell 2000 index up 3% for the week. Market sentiment was aided by comments from Federal Reserve Chair Jerome Powell, who stated in a speech at Jackson Hole, Wyoming, that “the time has come for policy to adjust”. In addition, the minutes to the FOMC’s July meeting noted the “vast majority” of participants said “it would likely be appropriate to ease policy at the next meeting”, reinforcing the view interest-rate cuts will begin at the next Fed meeting in September. In the bond markets, yields fell with the 2-Year and 10-year Treasury notes closing at yields of 3.91% and 3.81%, respectively. Investors now will look forward to the next inflation reading on Friday, the July personal consumption expenditures report. The report includes the preferred measure of inflation for the Fed, the core PCE Price index, which is expected at 2.7% on an annualized basis, up slightly from the 2.6% reading for June.

Update on Jobless Claims (from JP Morgan): Initial jobless claims have risen in recent months, averaging 236k since early June versus 213k in the first five months of 2024. Claims were volatile in July and, on two occasions, spiked to their highest levels since last August. This, in tandem with a weaker jobs report, stoked fears of a rapidly cooling labor market. Interestingly, a deeper dive into state-level data suggests two states are largely to blame for the swings in claims: Texas and Michigan. In these states, three of the last six weeks have shown week-to-week changes in initial claims that surpass one standard deviation in magnitude based on data back to 1988. In Michigan, larger temporary auto plant closures in July likely pressured more individuals to file for unemployment. In Texas, storm-related issues forced individuals out of work as the jump in claims coincided with Hurricane Beryl’s landfall in the state. These spikes proved temporary, however, and claims in both states have retraced lower. For the week ended Aug. 17, initial claims settled at 232k, higher than prints earlier this year but below the average 244k reported in the five years before the pandemic. While weekly prints may be volatile, long-term investors should focus on longer-term trends, which show a labor market that is slowing, but not one that is rapidly deteriorating. Beyond claims, BLS revisions released last week removed 818k jobs from payroll employment in March 2024. This suggests the labor market was weaker than reported in 2023, but also that strong productivity gains should be revised upward. In his speech at Jackson Hole, Chair Powell expressed more confidence in the disinflation process and noted the FOMC does “not seek or welcome” further cooling in the labor market. This cements a first rate cut in September, creating a sense of urgency for investors to lock in attractive yields before they move lower.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Factset, CNBC.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.