Market Recap – Week Ending Aug. 16

Stocks Rally After Stronger-Than-Expected Economic Data

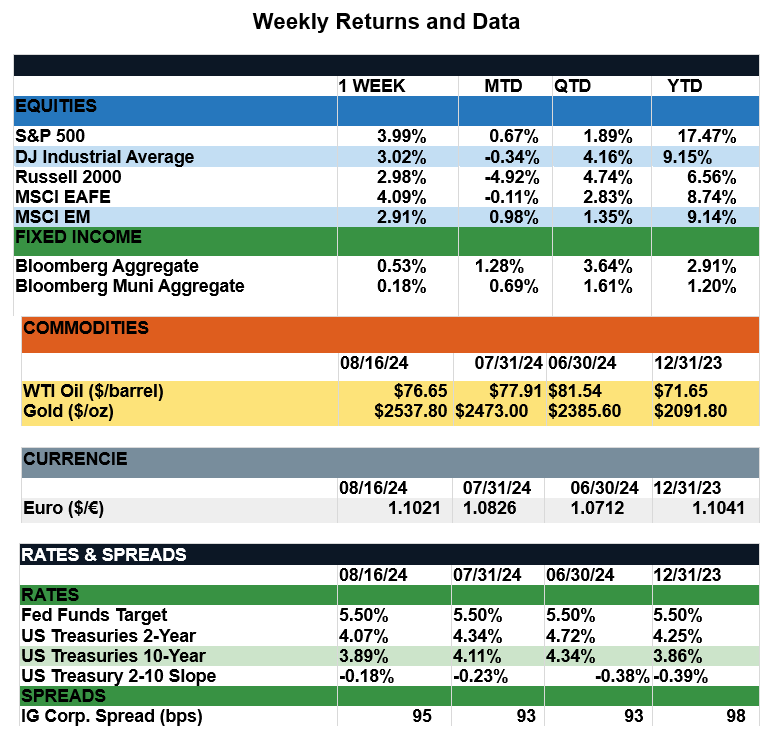

Overview: Global stacks rallied significantly in last week’s trade, benefitting from stronger-than-expected economic data as well as waning volatility. The S&P 500 index finished the week higher by 4%, while the MSCI EAFE (international developed index) finished the week higher by 4.1%. Both emerging market and small cap stocks saw a strong week of performance, tacking on 2.9% and 3%, respectively. Concerns of an economic growth slowdown were partially relieved as retail sales data come in well above consensus, expanding 1% for the month of July against expectations for a 0.4% increase. Separately, initial jobless claims, a real-time indicator for the labor market, came in lower than expected as did continuing jobless claims. On the inflation front, both headline and core CPI came in at consensus. For July, core prices rose 0.2%, and 3.2% on a year-over-year basis. This suggests a continuation of the disinflationary trends, a crucial input into the Fed’s monetary policy decisions going forward. In bonds, the 2-Year and 10- Year notes finished the week mostly unchanged with yields of 4.07% and 3.89%, respectively, as bonds added to their positive performance YTD. Looking forward to this week, the market will look forward to Federal Reserve Chair Jerome Powell’s Friday speech at the central bank’s annual symposium in Jackson Hole, Wyoming. With the markets expecting between 3-4 rate cuts between now and the end of the year, investors will pay close attention to Powell’s speech for any insights into the anticipated timing and magnitude of future rate cuts. In addition, minutes from the Fed’s July meeting are set to be released on Wednesday, followed by key housing data, jobless claims, as well as durable goods orders for the remainder of the week.

Update on the Fed and Interest Rates (from JP Morgan): Recent data have sent mixed signals about the U.S. economy, causing interest-rate expectations to fluctuate once again. Just two weeks ago, a weak jobs report sparked recession fears, and markets swiftly priced in an additional rate cut for this year. Since then, strong retail sales and low initial jobless claims readings helped alleviate these fears, and markets are now back to pricing in only three cuts in 2024. However, while short-term rate expectations dominate headlines, it is long-term rates that matter most to long-term investors. This week, we explore both market and Fed expectations of the longer-term, or “neutral,” federal funds rate. As of the most recent Summary of Economic Projections, the Fed’s “dot plot” projects the overnight rate will be 3.1% by the end of 2026, and not lower than 2.8% over the long run. Moreover, this number was revised higher, first in March and again in June, signifying the Fed thinks the economy can tolerate higher interest rates. This suggests that, barring any sort of economic collapse, the era of “free money” is likely over, and a more “normal” interest-rate environment, where real yields are positive, is upon us. Given this backdrop, investors may have to reconsider how they allocate capital. Higher bond yields could help investors achieve their income goals with less risk, while equity market quality will be more of a focus as companies combat higher borrowing costs.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Factset, CNBC.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.