Market Recap – Week Ending July 26

Positive GDP, PCE Data; Fed Meeting This Week

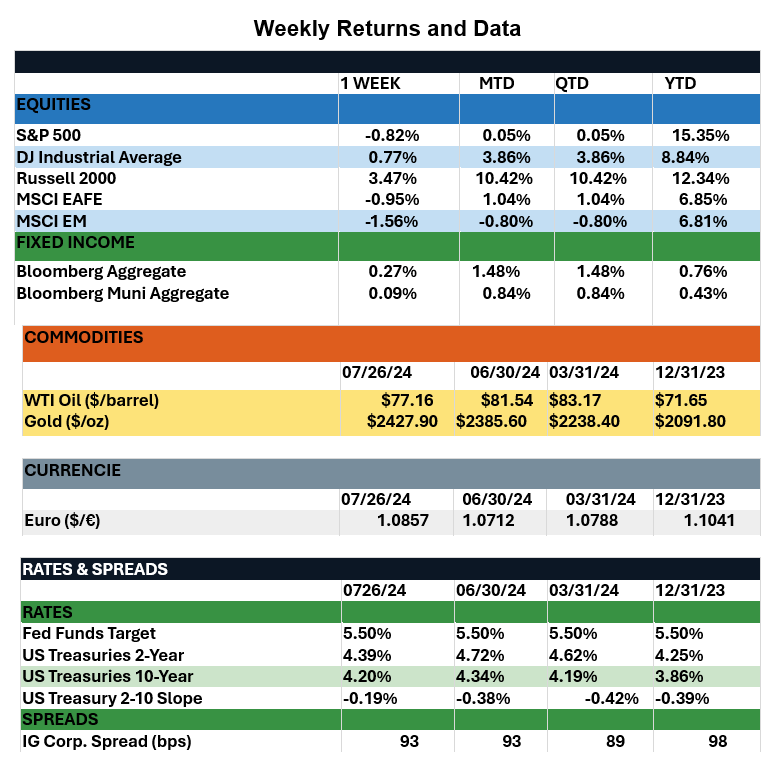

Overview: Major stock indices around the world fell last week as the S&P 500 experienced its first 2% down day in more than a year, leaving the index lower by 0.8%. International stocks followed suit, with the international developed index (MSCI EAFE) and emerging market index (MSCI EM) falling by 1% and 1.6%, respectively, for the week. Small-cap stocks continued their impressive run of outperformance, as the Russell 2000 gained more than 3.4% in total return for the week. The recent rotation in the markets throughout July has favored value stocks relative to growth stocks, and small-cap stocks over large-cap stocks. So far this month, the Russell 2000 is higher by more than 10%, followed by the Russell 1000 Value index, which is higher by more than 4%. In bonds, lower interest rates helped boost total returns, leaving both the taxable bond index (Bloomberg Aggregate) and the municipal bond index (Bloomberg Muni) in positive territory YTD. The big news last week came from the GDP report, which showed the U.S. economy expanded by 2.8% on an annualized basis, well above expectations for a more modest 2% increase. In addition, the Personal Consumption Expenditures (PCE) report was released on Friday, which showed core prices rose by 0.2% for the month of June, and 2.6% on a year-over-year basis, roughly in line with expectations. Looking ahead to this upcoming week, investors will have plenty to digest on the economic front as Wednesday brings the conclusion of the Federal Reserve’s meeting for July, followed by the nonfarm payrolls report on Friday. The markets aren’t expecting any changes to policy from the Fed this month but expect to hear Fed Chair Powell hint towards a 25-bps rate cut at the next meeting in September. On the jobs front, nonfarm payrolls are expected to increase by 175,000 for the month, while the unemployment rate is expected to remain unchanged at 4.1%.

Update on Earnings (from JP Morgan): While the recent political developments in Washington have grabbed headlines, it is important for investors not to lose sight of the fundamentals. The 2Q24 earnings season is underway, and by the end of last week, nearly half of the S&P 500’s market cap had already reported their earnings. Analysts are tracking pro-forma earnings per share (EPS) of $59.46 for 2Q24. If realized, this would represent a 5.3% q/q and 9.1% y/y growth. Of this annual change, most of the EPS growth (around 7.8% out of 9.1%) is projected to be driven by margin expansion (from 11.8% a year ago to 12.7%), while sales are expected to contribute 1.8%. Net buybacks are expected to have a negative contribution of 0.6%. From a sector standpoint, eight out of 11 sectors are expected to contribute positively to EPS growth. Technology leads yet again, with most of the earnings growth coming from increased sales as aggressive AI-related capex spending still dominates margin expansion. On the flip side, EPS growth in financials, the second-largest contributor, is projected to stem from margin expansion, primarily on the back of a rebound in investment banking and trading revenues. Of the remaining three sectors expected to drag down the EPS, energy is projected to have the most negative impact, as lower refining margins are expected to erode profitability of the sector.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Factset, CNBC.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.